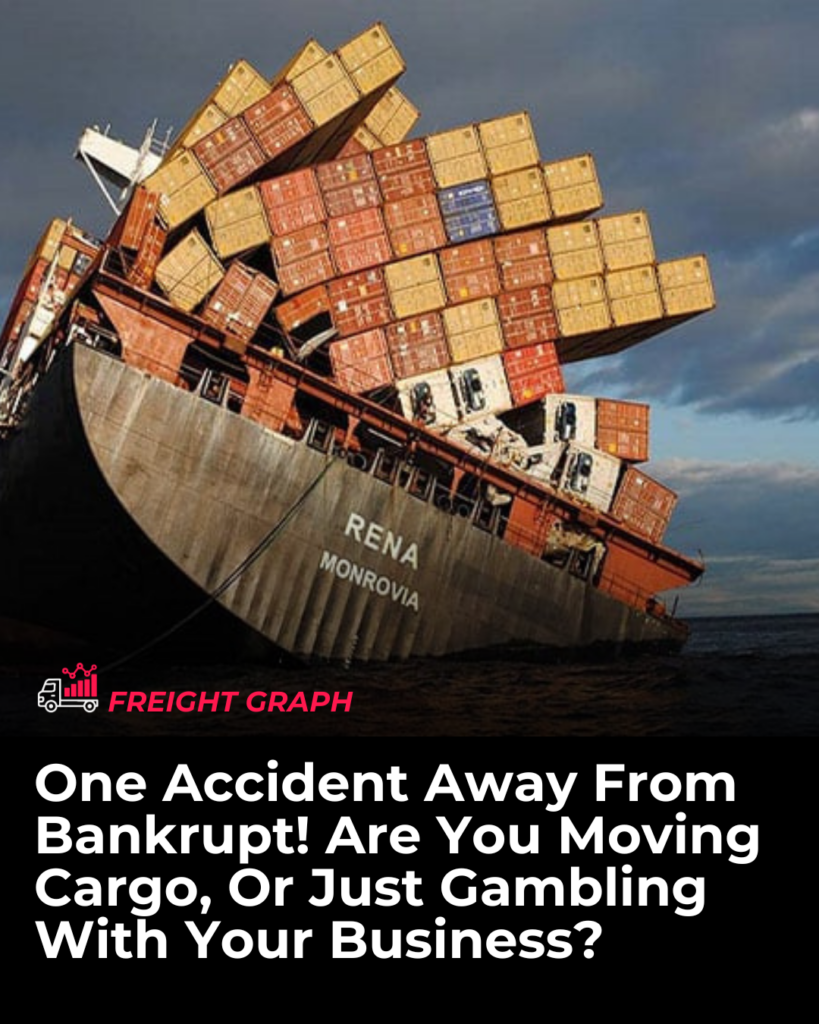

You booked the shipment. You chose a reliable carrier. You trusted the process.

Then the cargo was damaged — and you realized the carrier’s liability covers only a fraction of what your goods were worth.

This is not a rare scenario. It’s the reality thousands of importers and exporters face every year. And in 2026, with container losses at sea more than doubling year over year and cargo theft rising at record rates, the stakes have never been higher.

This guide breaks down exactly what cargo insurance for shippers means, why it matters, and how to get it right.

The Numbers Don’t Lie

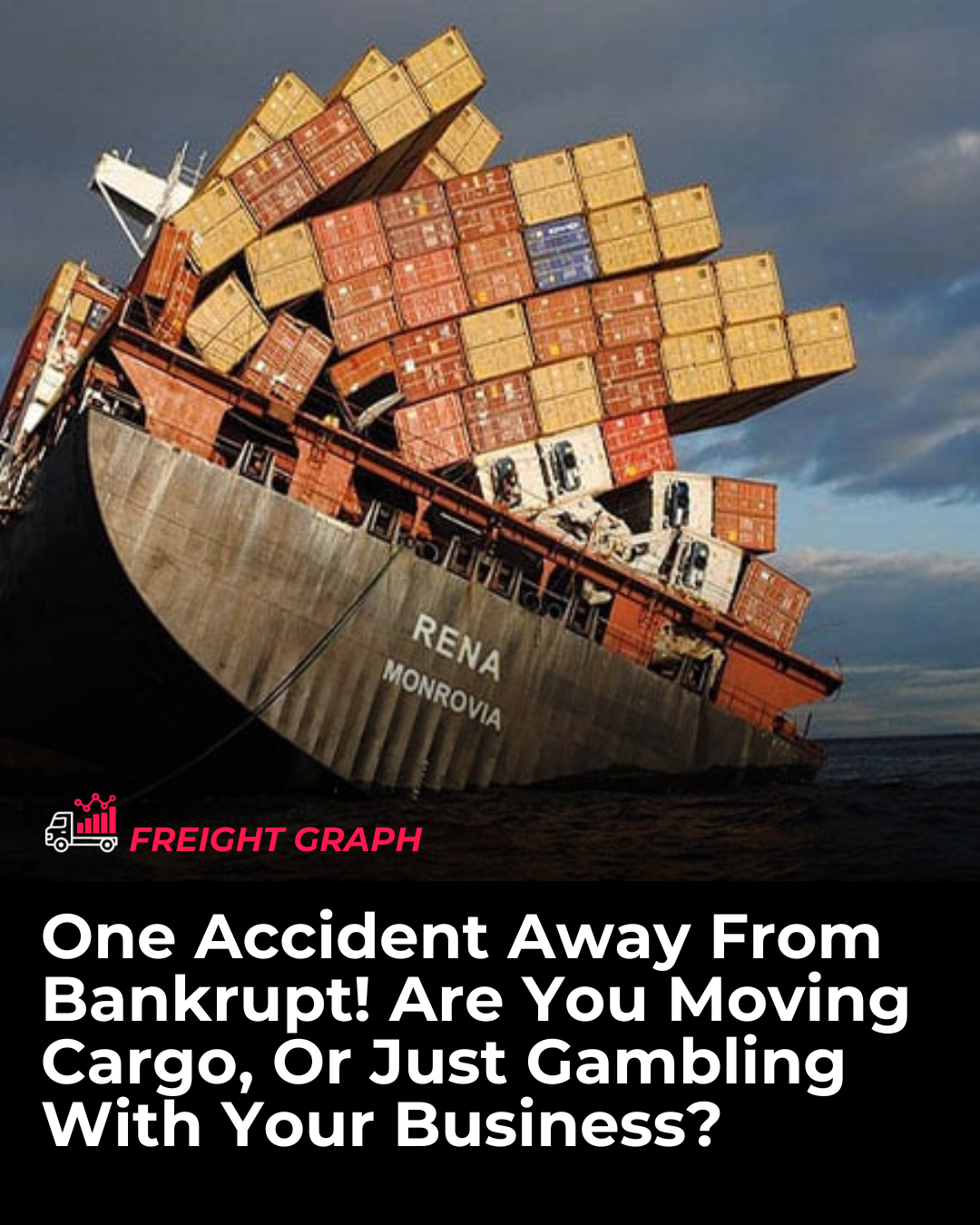

The World Shipping Council’s latest report recorded 1,478 containers lost at sea in 2025, up from 576 the year prior — a more than 150% increase in a single year.

One vessel loss alone — the MSC ELSA 3, which sank off the coast of Kochi, India in May 2025 — accounted for 43% of all containers lost globally that year.

And container losses are just one piece of the risk picture. Industry estimates suggest freight damage costs the global logistics industry between $50 billion and $60 billion annually. Meanwhile, cargo theft has become increasingly sophisticated, with organized criminal groups leveraging cyber tools and falsified documentation — with losses rising five-fold since late 2022.

The question is not whether something can go wrong. It’s whether you’re protected when it does.

Why Carrier Liability Is Not Enough

One of the most common and costly misconceptions in freight is this: “If the carrier damages my cargo, they’ll pay for it.”

That’s simply not how international shipping law works.

Carriers and freight forwarders only have limited liability. If an incident occurs, you may be faced with a long list of terms and conditions that are difficult for non-specialists to understand.

Under the international conventions that govern global shipping:

- Sea freight (Hague-Visby Rules): Carrier liability is capped at approximately $2 per kilogram or 666.67 SDR per package

- Air freight (Montreal Convention): Limited to roughly 22 SDR per kilogram

- Road freight (CMR Convention): Capped at around 8.33 SDR per kilogram

What does that mean in practice? If you’re shipping $50,000 worth of electronics in a 100 kg consignment, the carrier may legally owe you only a few hundred dollars.

Cargo insurance gives you the certainty that, if something goes wrong in transit, you will receive compensation based on the commercial invoice value. That’s the difference.

What Cargo Insurance Actually Covers

Cargo insurance protects your shipment from a wide range of risks that carrier liability simply doesn’t address:

- ✅ Fire and explosion

- ✅ Sinking, capsizing, or grounding

- ✅ Theft and piracy

- ✅ Loading and unloading damage

- ✅ Weather events (storms, floods, extreme cold/heat)

- ✅ General average (shared maritime sacrifice costs)

Even the most experienced freight forwarders cannot always prevent accidental damages during shipping. In such scenarios, insurance can cover the financial consequences, including claims from clients and legal expenses.

One area where many shippers get caught off guard is General Average. General average refers to collective damage to both a ship and its cargo. If a ship is in danger, it may be necessary to make sacrifices to safeguard the ship, its crew, and cargo — and all costs are shared proportionally between the ship owners and cargo owners. Without insurance, you may be billed for damage to cargo you never even owned.

The Three Main Types of Cargo Insurance

Not all cargo insurance policies are created equal. Here’s what you need to know:

| Type | What It Covers | Best For |

|---|---|---|

| All Risk | Broadest coverage — protects against most physical loss or damage | High-value or sensitive cargo |

| With Average (WA) | Partial losses at sea included | Standard ocean shipments |

| Free of Particular Average (FPA) | Only total losses or major perils | Durable, low-value bulk cargo |

All-Risk cargo insurance can typically be secured for a premium of around 0.3% to 0.5% of the goods’ commercial value — a small price for complete financial protection.

For most shippers, All Risk is the right choice. It eliminates guesswork about what’s covered when a claim arises.

How to Get Cargo Insurance: A Simple Checklist

Getting covered doesn’t have to be complicated. Follow these steps before every shipment:

- Determine the insured value — Use your commercial invoice value plus 10% (to cover profit and incidental costs)

- Choose the right coverage type — All Risk for most shipments

- Decide who arranges it — You can get it through your freight forwarder or directly from a marine insurer

- Get your Insurance Certificate before the cargo moves — this is your proof of coverage

- Document everything — photos, packing lists, weight declarations, and condition reports at origin

In 2026, premiums are rising 15–20% due to climate events, so locking in coverage early and reviewing your policy annually is more important than ever.

Who Needs Cargo Insurance?

The short answer: anyone who ships goods.

Whether you are handling shipments domestically or internationally, cargo insurance provides essential protection against the unpredictable risks of logistics and supply chain operations.

That includes:

- Importers and exporters

- E-commerce businesses shipping internationally

- Manufacturers sourcing raw materials overseas

- SMEs shipping LTL or LCL freight

Small and medium enterprises bear 85% of claims under $50,000 — making them among the most vulnerable, and the most underinsured.