Ocean freight rates in 2026 are at a crossroads. After months of volatility driven by the Iran war, a blockaded Strait of Hormuz, and surging fuel costs, several converging forces are now poised to reset the global container shipping market — for better and worse, depending on your position in the supply chain.

From a looming U.S.-Iran peace deal to General Rate Increases (GRIs), early peak season demand, and a growing vessel fleet, shippers and freight buyers need to understand each moving piece before it moves them. Here’s a full breakdown of what’s happening and what to expect.

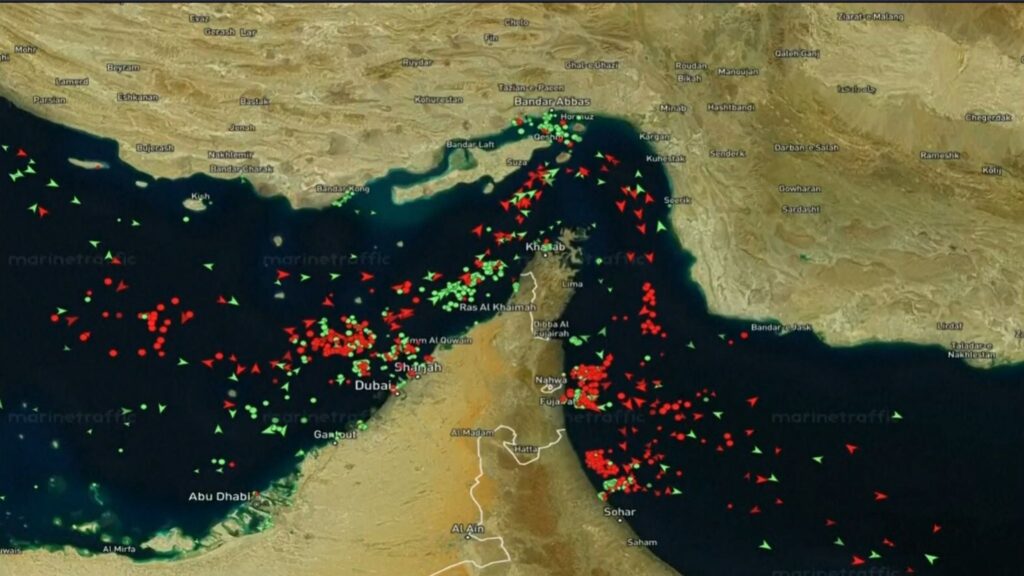

The Strait of Hormuz Peace Deal: A Game-Changer With a Long Fuse

The single most consequential development in ocean freight right now is the expected signing of a U.S.-Iran Memorandum of Understanding on June 19, 2026. The agreement is expected to reopen the Strait of Hormuz — which has been effectively closed to global shipping since shortly after the war erupted in late February — within approximately 30 days. The two sides will then have 60 days to negotiate a final peace accord.

President Trump has claimed the Strait will be fully open by the time of the signing, but experts are skeptical of an immediate normalization. The waterway has been further narrowed by Iranian mines, and some of the countries committed to the de-mining effort have expressed hesitation about participating until a final peace deal is in place.

According to Freightos Research Chief Judah Levine, estimates suggest it could take several weeks for daily vessel transits to return to even half of pre-war levels — and as long as six months for oil flows to fully normalize.

A priority by major economies to replenish strategic petroleum reserves, on top of mine-clearing delays, means the path back to normalcy is gradual. DHL Global Forwarding’s Middle East and Africa CEO Tobias Maier told customers to plan for disruptions, delays, and extra costs to persist for a sustained period — forecasting 4–6 months to normalization.

Bunker Fuel: Relief Is Coming, But Slowly

The war’s most direct and lasting impact on ocean freight rates has been through fuel. When the conflict began in late February, Brent crude spiked sharply, pushing Singapore VLSFO bunker fuel prices up as much as 68% compared to mid-February levels. At the war’s peak, Brent reached $126/barrel.

With the peace agreement, oil markets reacted immediately. Brent fell to around $83/barrel following the announcement — a significant drop from the $103–$113 range seen in May and June. However, as Freightos’s Levine noted, even once vessels exit the Strait, it takes roughly seven weeks for crude to arrive in the Far East — with an even longer timeline before refined products like bunker fuel become available.

This means:

- Emergency Fuel Surcharges (EFS) will ease for spot shipments, but the effect won’t be instantaneous.

- Bunker Adjustment Factors (BAFs) for Q3 contract shippers will remain elevated even as spot fuel costs decline, because BAF calculations lag by 30–60 days.

- War Risk Surcharges (WRS) will only be removed once insurers downgrade the region’s risk profile — which requires a sustained period of stability, not just a signing ceremony.

For shippers on annual contracts, the fuel cost relief from the peace deal will largely bypass the remainder of peak season.

Current Spot Rates: Where the Market Stands

Despite all the geopolitical drama, spot rates on the benchmark transpacific routes held relatively stable in the most recent week:

- Asia–U.S. West Coast: $4,836 per FEU (unchanged week-over-week), per the Freightos Baltic Index (FBX)

- Asia–U.S. East Coast: $6,558 per FEU (+4% week-over-week)

- Asia–Europe: Daily rates climbed approximately 10% this week, with vessels fully booked through month-end

These figures reflect the successful implementation of General Rate Increases (GRIs) and Peak Season Surcharges (PSSs) that went into effect June 1. Carriers are rolling containers and reducing allocations, reinforcing the price floor through mid-month — and making further increases in the near term likely to stick.

For context, transpacific rates to the U.S. West Coast are up roughly 40% since before the war started, while Asia–North Europe rates are up approximately 20%.

Peak Season Is Running Early — and Hot

The second major force driving ocean freight rates in 2026 is an unusually early and intense peak season.

Shippers are frontloading cargo in a race to beat three converging cost pressures:

- July 1 Bunker Adjustment Factor increases — Annual contract BAFs will reset at higher rates reflecting Q2 fuel costs

- Asian manufacturer price hikes — Manufacturers in China and across Southeast Asia are raising FOB prices as petroleum-derived input costs (plastics, synthetics, chemicals) rise with oil

- Potential tariff escalations — With Section 122 tariffs (10%) still in place alongside Section 301 China-specific duties, importers are hedging forward

This demand pull-forward has created a booking surge in June, with carriers reporting vessels fully booked through end of month. According to Lloyd’s List, Drewry flagged this as an “early peak season” dynamic, noting demand being pulled forward ahead of expected July 1 BAF increases.

The early surge does carry a risk for carriers: if bookings top out in June, shippers may show resistance to further increases in July — potentially capping the typical summer rate escalation before it can fully materialize.

The Long-Term Downward Pressure: Fleet Overcapacity

Once the war-related fuel shock fades, a structural market force waiting in the wings could aggressively push ocean freight rates lower: vessel overcapacity.

Between 2020 and 2023, shipping lines placed massive newbuilding orders to capitalize on pandemic-era profits. That order book — representing more than 7 million TEUs of additional capacity — has been delivered across 2024 and 2026, pushing the global fleet into a structural surplus. Analysts at Maritime Gateway note the supply-demand ratio on main East-West routes shows a 10%+ capacity surplus — and historically, even a 5% surplus is enough to significantly drive rates down.

During the conflict, this oversupply was masked by two factors:

- The effective closure of the Hormuz and Red Sea routes reduced available capacity by approximately 12%, per MPC Container Ships CEO Constatin Baack

- Slow steaming due to higher fuel costs absorbed another 2% of capacity

As Levine summarized: once fuel prices normalize, freight rates will face renewed downward pressure from a growing fleet — the same trend that was underway before the war disrupted everything. And if a peace deal enables carriers to return to Red Sea routing at scale, that downward pressure will be even more pronounced.

What Shippers Should Do Now

Given the complexity of the current market, here are the key strategic levers for shippers:

1. Don’t wait on fuel cost relief. The peace deal is a medium-term positive for rates, but it won’t lower your Q3 contracted BAFs or help with July bookings. Plan accordingly.

2. Lock in capacity now if you have near-term volume. Vessels are fully booked through June. If you have July volume, engage your forwarder or carrier immediately — rolling and allocation cuts are already happening.

3. Reassess your routing strategy. Cape of Good Hope reroutes added 10–14 days per voyage on Asia–Europe and Asia–U.S. East Coast lanes. Monitor Hormuz reopening closely; a fully restored Suez/Hormuz corridor would meaningfully reduce transit times and effective carrier costs in Q4.

4. Prepare for rate volatility in both directions. Near-term rate increases look likely through mid-June. But as fleet capacity reasserts itself in H2 2026 and fuel costs ease, the direction could reverse sharply for spot shipments.

5. Use real-time rate intelligence. In a market shifting this fast, static rate cards and quarterly benchmarks are insufficient. Platforms like FreightGraph give you live visibility into transpacific and Asia-Europe rate trends so you can time procurement decisions with market data, not guesswork.

The Bottom Line

Supply chain normalcy in 2026 is still likely months away. The Strait of Hormuz peace deal is a genuine turning point, but its benefits will take time to flow through to fuel costs, carrier operations, and ultimately container rates.

In the near term, the early peak season and mid-month GRI implementations are keeping rates elevated. In the medium term, falling fuel costs and a growing vessel fleet will push rates back toward — and potentially below — pre-war levels. And in the long run, the structural overcapacity in the container shipping market remains the dominant pricing force once geopolitical headwinds clear.

For shippers, that means 2026 will reward those who act with data, not gut instinct. The window for peak season capacity is closing. The window for more favorable H2 rates may be opening sooner than the market expects.

Sources:

- FreightWaves – Coming weeks will see multiple factors reset ocean rates

- Freightos Weekly Freight Update – June 16, 2026

- Lloyd’s List – Hormuz crisis side effect: a sharp rise in container shipping rates

- Seavantage – Strait of Hormuz Crisis 2026: Full Timeline & Ocean Freight Impact

- SinoShipment – Strait of Hormuz Reopens: Impact on Shipping from China

- Maritime Gateway – Container Shipping Forecast 2026

- FreightPerspectives – Freight Rates Will Remain High Despite the Strait of Hormuz Reopening